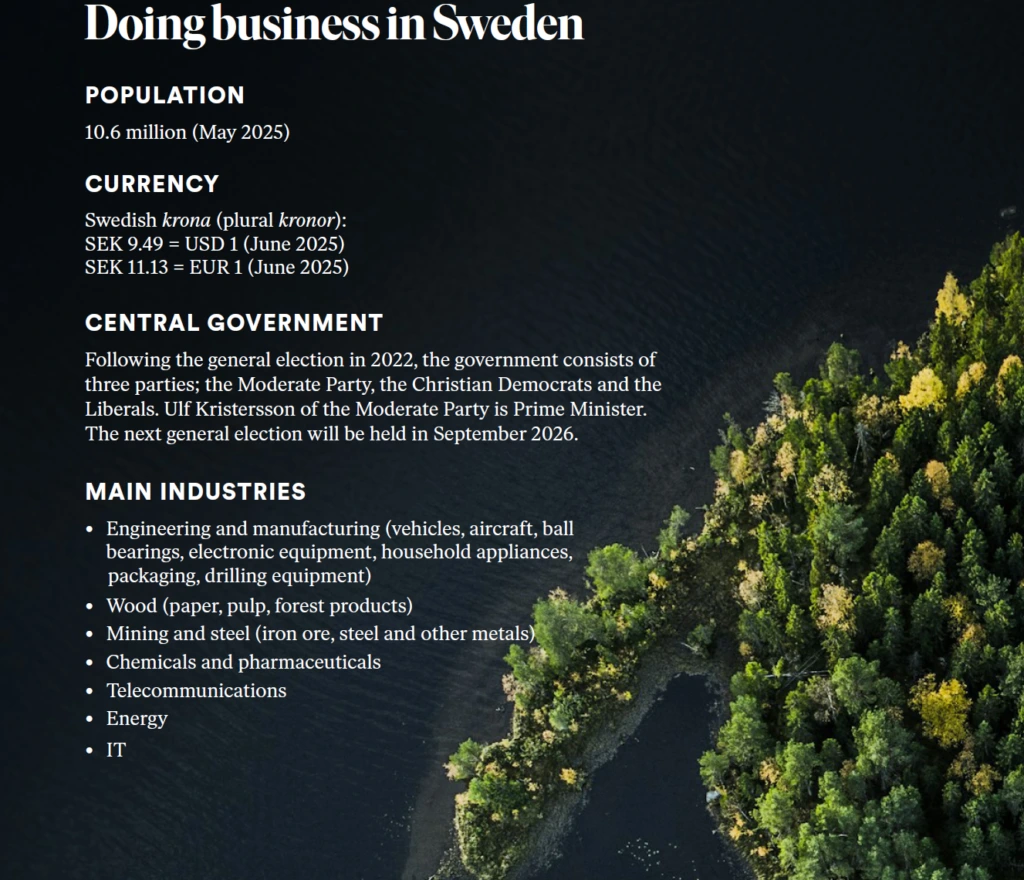

Sweden remains one of Europe’s most stable and attractive markets for doing business in 2025, offering EU market access, strong legal certainty, transparent governance, and a highly developed digital and innovation ecosystem. Foreign investment is generally encouraged, supported by competitive corporate taxation and robust protection of property and contractual rights. However, recent regulatory developments—particularly foreign direct investment screening, EU foreign subsidy rules, and competition oversight—mean that successful market entry now requires earlier planning and stronger compliance readiness. Sweden rewards long-term, well-governed businesses that align with its high standards in corporate governance, taxation, employment, and regulatory transparency.

Doing Business in Sweden 2025 — Key Points at a Glance

🇸🇪 Business & Investment Climate

- EU member since 1995; EU law fully integrated into Swedish law

- No exchange controls or currency restrictions

- Foreign ownership generally unrestricted

- Strong public institutions, political stability, and rule of law

🏛️ Legal & Regulatory Framework

- Legal system based on statute law and case law

- Signatory to major international conventions (including CISG)

- Courts are efficient; arbitration is highly developed

- Stockholm is a leading global arbitration venue

🌍 Foreign Investment & Control

- Foreign investment encouraged, but FDI screening applies

- Mandatory notification for investments in security-sensitive or strategic sectors

- Applies regardless of investor nationality, including some intra-group transactions

- Standstill obligation until approval is granted

🏢 Business Structures

- Most common entity: Limited Liability Company (AB)

- Minimum share capital:

- Private AB: SEK 25,000

- Public AB: SEK 500,000

- Shareholders have limited liability

- Clear rules on board duties, director liability, and governance

🤝 M&A and Competition

- Private M&A largely contract-driven

- Public takeovers subject to mandatory bid rules

- Merger control applies if Swedish turnover thresholds are exceeded

- Large transactions may also trigger EU Foreign Subsidies Regulation (FSR)

💼 Taxation

- Corporate income tax: 20.6% (flat rate)

- Participation exemption for qualifying dividends and capital gains

- Loss carry-forward generally unlimited (subject to ownership rules)

- Interest deductibility limited by EBITDA-based rules

- Transfer pricing aligned with OECD arm’s-length principle

👩💼 Employment & Workforce

- Employment regulated by law and collective bargaining agreements

- Strong employee protections and union influence

- Minimum 25 days paid annual leave

- Employers pay approx. 31.4% social security contributions

- Termination requires objective grounds and procedural compliance

🧠 Intellectual Property & Innovation

- Strong protection for patents, trademarks, designs, copyrights, and trade secrets

- IP framework fully aligned with EU regulations

- Efficient enforcement through courts and authorities

⚖️ Dispute Resolution

- Well-functioning court system with predictable outcomes

- Arbitration awards widely enforceable under the New York Convention

- Costs generally follow the outcome of litigation

Want the Full Picture?

This summary highlights only the most critical considerations.

For detailed guidance on corporate structures, taxation, employment law, M&A, IP protection, and dispute resolution, read the full report:

👉 Doing Business in Sweden 2025 – Vinge

(Official publication by Advokatfirman Vinge KB)

You can read the full article at:

chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/https://www.vinge.se/media/3dwneynu/doing-business-in-sweden-2025.pdf